Everything you should know about the New Plastic Tax

In January 2023, the tax on the manufacture, import or intra-community acquisition of non-reusable plastic packaging incorporating plastic will come into force. We are talking about the plastic tax, which is part of one of the measures included in the Law on Waste and Contaminated Soils for a Circular Economy, and which will tax with 0.45 euros/kg the non-recycled plastic content in non-reusable packaging.

This tax is generating a lot of controversy in an industry punished by multiple factors that are shaking an already unstable market. In response to the multitude of queries we are receiving about the new plastic tax, we will try to clarify what it is and what it consists of.

- Definition:

The IPNR is an indirect tax levied on the use in Spanish territory of non-reusable packaging containing non-recycled plastic. The standard that establishes which containers are or are not reusable is the UNE-EN 13429:2005 standard on «Containers and packaging. Reuse».

Entry into force:

This tax, which is regulated in Chapter I of Title VII of Law 7/2022, of April 8, will enter into force on January 1, 2023.

- Taxable event:

The taxable event of the tax falls on the following activities:

* The manufacture of plastics.

* Import of plastics from outside the EU.

* Intra-community acquisition of plastics.

The tax is paid only once, and is payable by the person who first introduces the film into the Spanish market.

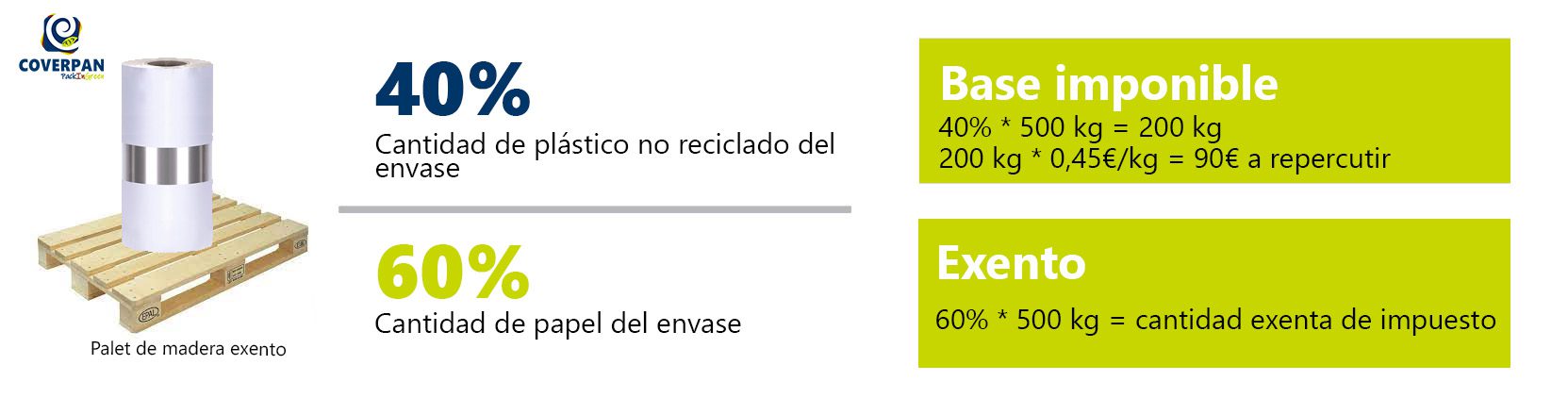

How is the tax calculated?

The applicable tax rate is 0.45 euros per kilogram of non-recycled plastic contained in non-recyclable plastic packaging.

To calculate the amount of the new plastic tax, the amount of non-recycled plastic contained in the packaging will be used as the taxable base and the tax rate will be 0.45 €/kg.

We leave you an example of this calculation with a reel that is composed of paper and non-recycled plastic:

Objective Scope of the New Plastics Tax. IPNR

The IPNR will be applied throughout Spain to:

- Packaging that, containing non-recycled plastic, is not reusable.

- Semi-finished plastic products intended to obtain packaging, such as preforms and thermoplastic sheets.

- Products containing non-recycled plastic intended to enable the closure, marketing or presentation of non-reusable packaging.

For the purposes of the IPNR, packaging is considered to be any product intended to perform the function of containing, protecting, handling, distributing and presenting goods. All disposable articles used for the same purpose are also considered packaging. Within this concept, and therefore affected by the IPNR, are included sales or primary packaging, collective or secondary packaging and transport or tertiary packaging.

Who will have to pay the new tax?

The accrual and taxpayers differ depending on whether the taxable event is the manufacture, importation, intra-Community acquisition or irregular possession of products that are part of the objective scope:

- The manufacturer is the taxpayer in the manufacturing process and the accrual of the tax occurs with the first delivery or making available, in Spanish territory, of the manufactured products. Or with the total or partial collection of the price, if payments are made in advance of the delivery or availability of the manufactured products.

- The importer is the taxpayer on the import and the accrual of the tax occurs at the time the import duties are accrued in accordance with the customs legislation.

- In the intracommunity acquisition, the taxpayer is the intracommunity acquirer, and the accrual of the tax occurs on the 15th day of the month following the month in which the transport or shipment to the acquirer begins or at the time of the issuance of the invoice, if earlier.

- Whoever possesses, commercializes, transports or uses them is the taxpayer in the irregular possession. The accrual of the tax occurs at the moment of the irregular introduction and, if not known, in the oldest liquidation period not prescribed, unless it is proved that it corresponds to another.

For more information on the Plastic Tax Law, please consult the BOE (Official Gazette of the Government of Spain)

Which plastic containers are exempt from the tax?

For the purposes of this tax, industries such as pharmaceuticals that market health products such as medicines, prostheses or surgical instruments are exempt from the tax. Also exempted are plastics for agricultural use for certain uses such as for silage or cereal fodder.

Exports are exempt and recycled plastics are excluded provided they are AENOR accredited.

What can we do to minimize the impact of this tax?

One of the queries we are receiving the most is “How can I get the exemption from the payment of the plastic tax?” and our answer is clear, applying the Ecodesign on packaging; and for this you can take several measures that we tell you below:

1. Reduce the thickness of the package. By lowering the micronage, reducing the size of the package or reducing the amount of ink on the package.

2. Replace the plastic material with a compostable material.

Our PackInGreen packaging is made from paper, cellulose and film combinations based on regenerated cellulose; and according to Directive (EU) 2019/904 (SUPD Directive) states that:

– “Cellulose extracted from wood meets the definition of natural polymer (section 2.1.3 (i) Non-chemically modified natural polymers of the Commission’s Guidelines issued on May 31, 2021).”

– “Regenerated in the form of cellophane, lyocell and cellulose film, is not considered chemically modified, as the resulting polymers do not constitute a chemical modification of the incoming polymer.”

Therefore, our PackInGreen films are not considered as plastics. As they are not plastics, our films should be exempt from the new tax defined in Law 07/2022 of April 8th, on waste and contaminated soils.

The sustainability of packaging is no longer an option, it is a legal obligation, and its compliance affects not only the manufacture of these, but also its end of life and its management as waste.

Check our PackInGreen solutions catalog here

Frequently Asked Questions

How to prove the exemption of medical device packaging?

The purchaser of the packaging must send a declaration of the use of its packaging to its supplier.

A Spanish buyer buys packaging manufactured in Spain and then sends it abroad, will he pay the tax?

Yes, he pays the tax to the manufacturer and when he accredits the shipment abroad, he can request the refund to the tax agency.

Will a Spanish buyer who purchases packaging from a foreign supplier pay the tax?

Yes, when importing at customs or intra-community acquisition by means of self-assessment.

When is a container considered to be reusable?

When it has been conceived, designed and marketed for multiple circuits or to be refilled or reused for the same purpose for which it was conceived or designed. UNE-EN 13429:2005 Standard on «Containers and packaging. Reuse».

What type of recycling is exempt?

Both post-industrial and post-consumer mechanical recycling.

What are the requirements for recycling to be exempt?

It must be certified by an entity accredited by AENOR.